Most likely you’ve read the tantalizing stories of big gains from investing in cryptocurrencies. Someone who invested $1,000 into bitcoins five years ago would have over $85,000 in value now. Alternatively, someone who invested in bitcoins three months ago would have seen their investment lose 20% in value. Beyond the big price fluctuations, currency holders are possibly exposed to fraud, bad business practices, and even risk losing their holdings altogether if they are careless in keeping track of the all-important currency keys.

It’s certain that beyond the rewards and risks, cryptocurrencies are here to stay. We can’t ignore how they are changing the game for how money is handled between people and businesses.

Some Advantages of Cryptocurrency

- Cryptocurrency is accessible to anyone.

- Decentralization means the network operates on a user-to-user (or peer-to-peer) basis.

- Transactions can completed for a fraction of the expense and time required to complete traditional asset transfers.

- Transactions are digital and cannot be counterfeited or reversed arbitrarily by the sender, as with credit card charge-backs.

- There aren’t usually transaction fees for cryptocurrency exchanges.

- Cryptocurrency allows the cryptocurrency holder to send exactly what information is needed and no more to the merchant or recipient, even permitting anonymous transactions (for good or bad).

- Cryptocurrency operates at the universal level and hence makes transactions easier internationally.

- There is no other electronic cash system in which your account isn’t owned by someone else.

On top of all that, blockchain, the underlying technology behind cryptocurrencies, is already being applied to a variety of business needs and itself becoming a hot sector of the tech economy. Blockchain is bringing traceability and cost-effectiveness to supply-chain management — which also improves quality assurance in areas such as food, reducing errors and improving accounting accuracy, smart contracts that can be automatically validated, signed and enforced through a blockchain construct, the possibility of secure, online voting, and many others.

Like any new, booming marketing there are risks involved in these new currencies. Anyone venturing into this domain needs to have their eyes wide open. While the opportunities for making money are real, there are even more ways to lose money.

We’re going to cover two primary approaches to staying safe and avoiding fraud and loss when dealing with cryptocurrencies. The first is to thoroughly vet any person or company you’re dealing with to judge whether they are ethical and likely to succeed in their business segment. The second is keeping your critical cryptocurrency keys safe, which we’ll deal with in this and a subsequent post.

Caveat Emptor — Buyer Beware

The short history of cryptocurrency has already seen the demise of a number of companies that claimed to manage, mine, trade, or otherwise help their customers profit from cryptocurrency. Mt. Gox, GAW Miners, and OneCoin are just three of the many companies that disappeared with their users’ money. This is the traditional equivalent of your bank going out of business and zeroing out your checking account in the process.

That doesn’t happen with banks because of regulatory oversight. But with cryptocurrency, you need to take the time to investigate any company you use to manage or trade your currencies. How long have they been around? Who are their investors? Are they affiliated with any reputable financial institutions? What is the record of their founders and executive management? These are all important questions to consider when evaluating a company in this new space.

Would you give the keys to your house to a service or person you didn’t thoroughly know and trust? Some companies that enable you to buy and sell currencies online will routinely hold your currency keys, which gives them the ability to do anything they want with your holdings, including selling them and pocketing the proceeds if they wish.

That doesn’t mean you shouldn’t ever allow a company to keep your currency keys in escrow. It simply means that you better know with whom you’re doing business and if they’re trustworthy enough to be given that responsibility.

Keys To the Cryptocurrency Kingdom — Public and Private

If you’re an owner of cryptocurrency, you know how this all works. If you’re not, bear with me for a minute while I bring everyone up to speed.

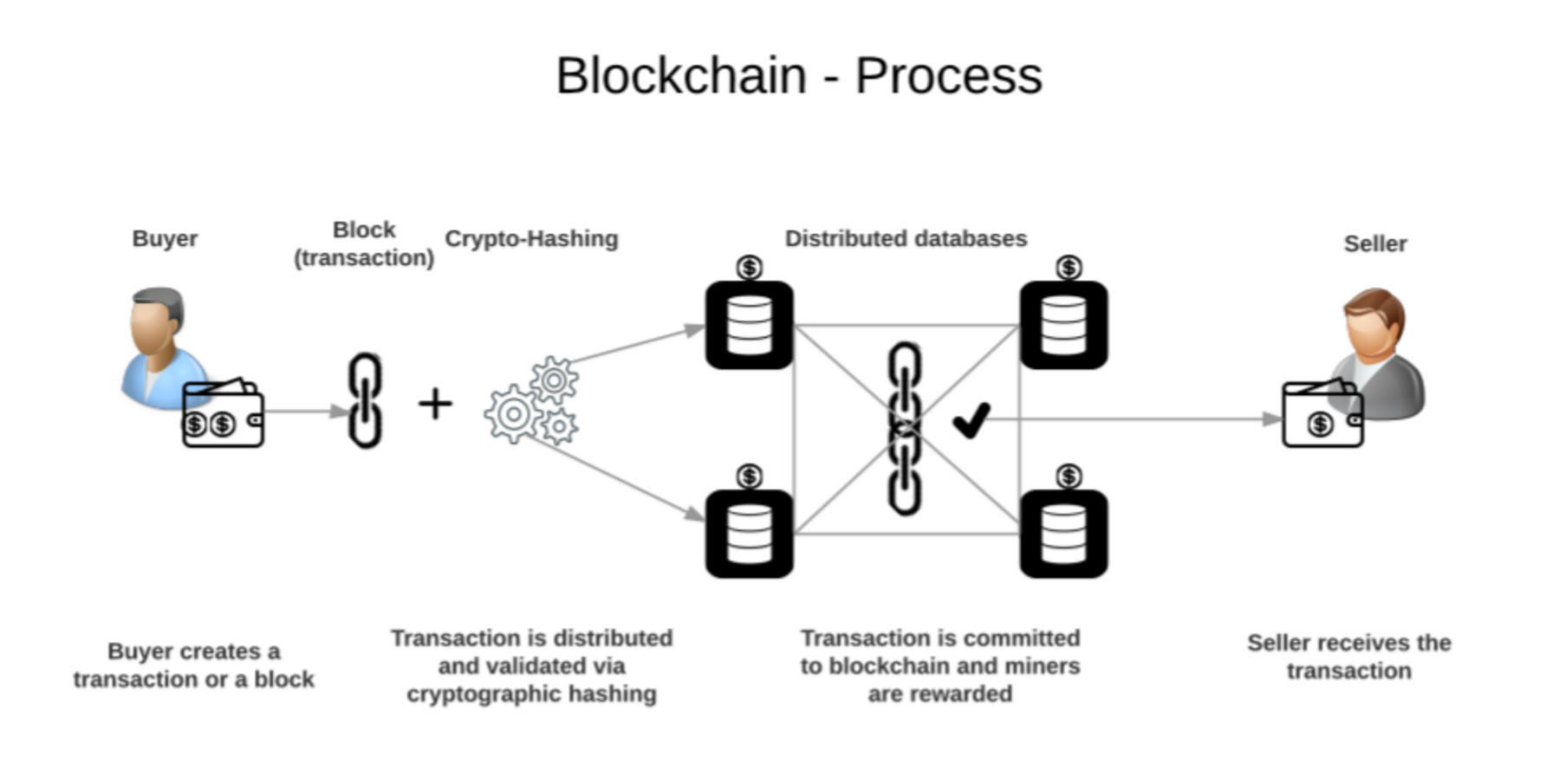

Cryptocurrency has no physical manifestation, such as bills or coins. It exists purely as a computer record. And unlike currencies maintained by governments, such as the U.S. dollar, there is no central authority regulating its distribution and value. Cryptocurrencies use a technology called blockchain, which is a decentralized way of keeping track of transactions. There are many copies of a given blockchain, so no single central authority is needed to validate its authenticity or accuracy.

The validity of each cryptocurrency is determined by a blockchain. A blockchain is a continuously growing list of records, called “blocks”, which are linked and secured using cryptography. Blockchains by design are inherently resistant to modification of the data. They perform as an open, distributed ledger that can record transactions between two parties efficiently and in a verifiable, permanent way. A blockchain is typically managed by a peer-to-peer network collectively adhering to a protocol for validating new blocks. Once recorded, the data in any given block cannot be altered retroactively without the alteration of all subsequent blocks, which requires collusion of the network majority. On a scaled network, this level of collusion is impossible — making blockchain networks effectively immutable and trustworthy.

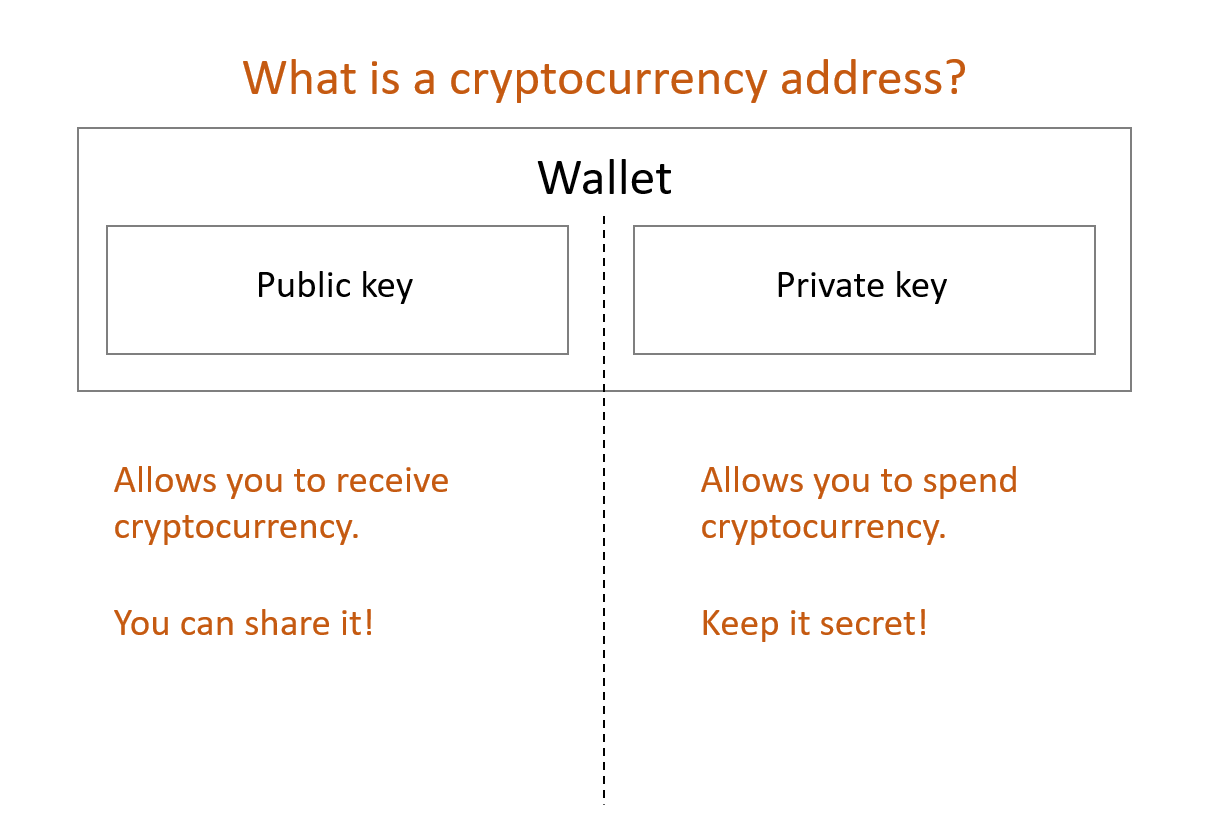

The other element common to all cryptocurrencies is their use of public and private keys, which are stored in the currency’s wallet. A cryptocurrency wallet stores the public and private “keys” or “addresses” that can be used to receive or spend the cryptocurrency. With the private key, it is possible to write in the public ledger (blockchain), effectively spending the associated cryptocurrency. With the public key, it is possible for others to send currency to the wallet.

Cryptocurrency “coins” can be lost if the owner loses the private keys needed to spend the currency they own. It’s as if the owner had lost a bank account number and had no way to verify their identity to the bank, or if they lost the U.S. dollars they had in their wallet. The assets are gone and unusable.

The Cryptocurrency Wallet

Given the importance of these keys, and lack of recourse if they are lost, it’s obviously very important to keep track of your keys.

If you’re being careful in choosing reputable exchanges, app developers, and other services with whom to trust your cryptocurrency, you’ve made a good start in keeping your investment secure. But if you’re careless in managing the keys to your bitcoins, ether, Litecoin, or other cryptocurrency, you might as well leave your money on a cafe tabletop and walk away.

What Are the Differences Between Hot and Cold Wallets?

Just like other numbers you might wish to keep track of — credit cards, account numbers, phone numbers, passphrases — cryptocurrency keys can be stored in a variety of ways. Those who use their currencies for day-to-day purchases most likely will want them handy in a smartphone app, hardware key, or debit card that can be used for purchases. These are called “hot” wallets. Some experts advise keeping the balances in these devices and apps to a minimal amount to avoid hacking or data loss. We typically don’t walk around with thousands of dollars in U.S. currency in our old-style wallets, so this is really a continuation of the same approach to managing spending money.

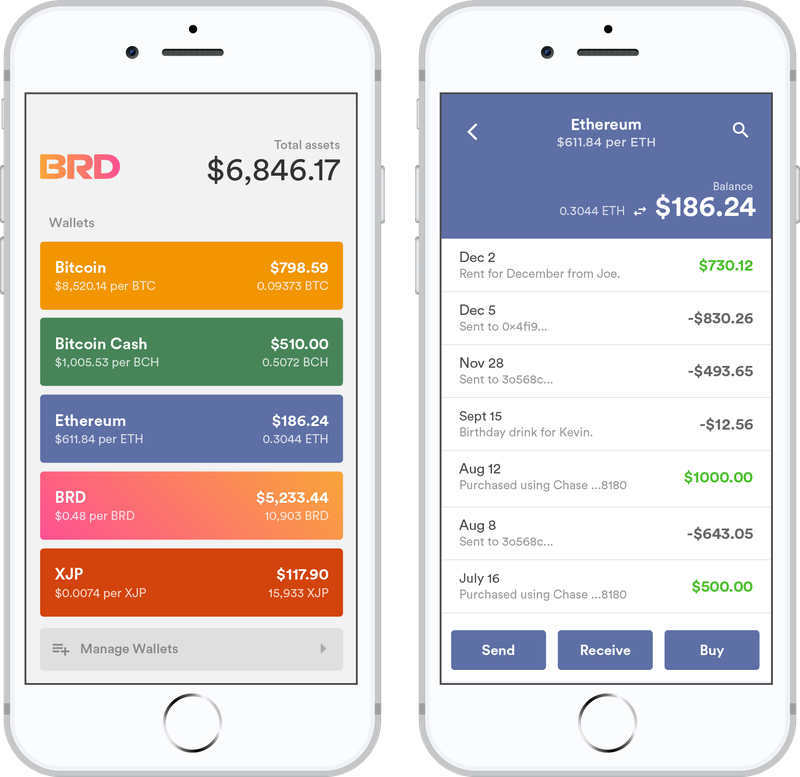

A “hot” wallet, the Bread mobile app

Some investors with large balances keep their keys in “cold” wallets, or “cold storage,” i.e. a device or location that is not connected online. If funds are needed for purchases, they can be transferred to a more easily used payment medium. Cold wallets can be hardware devices, USB drives, or even paper copies of your keys.

A “cold” wallet, the Trezor hardware wallet

A “cold” wallet, the Ledger Nano S

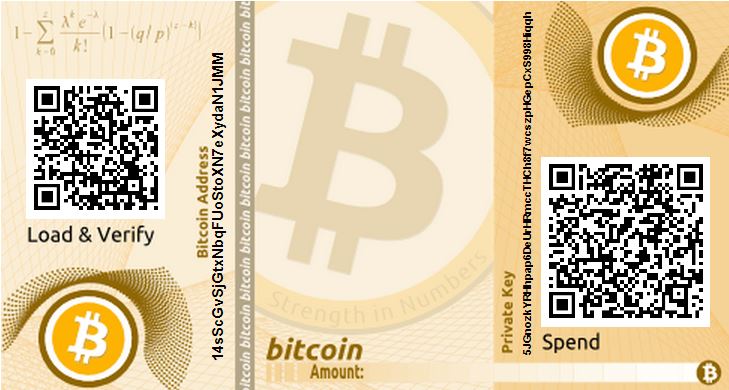

A “cold” Bitcoin paper wallet

Wallets are suited to holding one or more specific cryptocurrencies, and some people have multiple wallets for different currencies and different purposes.

A paper wallet is nothing other than a printed record of your public and private keys. Some prefer their records to be completely disconnected from the internet, and a piece of paper serves that need. Just like writing down an account password on paper, however, it’s essential to keep the paper secure to avoid giving someone the ability to freely access your funds.

How to Keep your Keys, and Cryptocurrency Secure

In a post this coming Thursday, Securing Your Cryptocurrency, we’ll discuss the best strategies for backing up your cryptocurrency so that your currencies don’t become part of the millions that have been lost. We’ll cover the common (and uncommon) approaches to backing up hot wallets, cold wallets, and using paper and metal solutions to keeping your keys safe.

In the meantime, please tell us of your experiences with cryptocurrencies — good and bad — and how you’ve dealt with the issue of cryptocurrency security.